[ad_1]

By 2023, there will be around 350 million linked automobiles on the street. What can the insurance policies marketplace do about it? It turns out that fairly a little bit, as automotive companies, introducing the newest technological developments, are enabling new approaches to combine driver habits. This is of great great importance in the context of generating offers, but not only. At stake is to retain the placement and competitiveness in the field of motor coverage.

The automotive and automobile coverage industries are shifting

The automotive market place is previously going through alterations pushed by innovative systems. Additional normally than not, these are based mostly on the software package-outlined motor vehicle (SDV) pattern.

If the motor vehicle is outfitted with embedded connectivity, it is able to offer very comprehensive car and driver conduct information, these as:

● sudden acceleration or braking,

● taking sharp turns,

● peak activity occasions (nighttime drivers are extra susceptible),

● regular pace and acceleration,

● accomplishing risky maneuvers.

BBI & UBI and ADAS

Actions-centered (pay back-how-you-push) and use-centered insurance coverage – UBI – (shell out-as-you-push) are the future of auto insurance plans. Meanwhile, as vehicles turn out to be smarter, much more connected, and automatic, insurers evaluate not only the driver’s habits but also the car s/he is driving. This analysis will take into account, between other items, the quantity of sophisticated driver aid programs (ADAS) that have an impact on the safety of the vehicle’s occupants.

Autonomous vehicles

And Deloitte analysts be aware that self-driving (AV) vehicles, which are an intriguing novelty now but will in time be a common on par with human-driven cars, are also possible to force basic modifications in insurers’ product ranges, as in the possibility evaluation, pricing, and business styles.

Related autos

Modify is now going on, and it will turn into even much more pronounced in the a long time ahead. IoT Analytics predicts that by 2025, the total quantity of IoT devices throughout the world will exceed 27 billion. Plus, gurus predict that there will be 7.2 billion energetic smartphones and extra than 400 million related cars on the highway through the same interval.

This all evidently reveals that we are in an solely diverse fact than we have been just a couple or a dozen years ago. Automobile insurers need to have an understanding of this if they want to retain their foothold.

Telematics systems are an clear stage into the future of the insurance policy field

Coverage providers have been featuring use-based mostly and conduct-centered products for years dependent on details from possibly additional units or cellular apps. This is a quickly-developing products location since the UBI market place is predicted to be value much more than $105 billion in 2027, up 23.61% per year.

The very best placement in this arena is attained by organizations that started investing in telematics know-how early and now can get pride in perfectly-developed telematics products and solutions.

We are conversing about manufacturers such as Point out Farm®, Nationwide, Allstate, and Progressive. Yet at the exact same time, corporations that considered telematics a passing development and consequently didn’t invest in it missing a pretty massive volume of sector share. The result? Now they have to catch up and race to continue to keep up with the competition.

TSPs fully grasp the prospective of connected auto data

Insuring firms are not the only ones who figure out the great importance of utilizing their telematics-centered options. Telematics expert services suppliers have an understanding of that benefit as properly, so they spend in developing out new capabilities of their products and solutions.

This is the situation with GEICO, the 2nd-greatest car insurance company in the U.S. (suitable after Progressive). As Ajit Jain, vice president of Insurance policy Operations at Berkshire Hathaway claims: GEICO had evidently skipped the business and were late in phrases of appreciating the worth of telematics. They have woken up to the simple fact that telematics plays a big part in matching price to possibility. They have a number of initiatives, and, hopefully, they will see the gentle of day right before, not too extensive, and that’ll enable them to catch up with their rivals, in conditions of the challenge of matching fee to danger.

Telematics firms see likely in partnering with the coverage marketplace

Insurance policies corporations are not the only kinds who identify the great importance of implementing new info-pushed engineering remedies. The marriage is two-way, as telematics business representatives, in turn, are keen to make investments in collaboration with insurers and set the shopper from this industry sector first.

For case in point, Cambridge Mobile Telematics (CMT), the world’s major telematics company, has a short while ago introduced the expansion of its proprietary DriveWell® telematics system to networked motor vehicles. Their flagship application has previously collected sensor information from tens of millions of IoT devices, such as smartphones, tags, in-car cameras, third-social gathering devices, and so on. From now on, that scope proceeds to broaden by particularly which includes connected cars to build a unified check out of driver and car behavioral hazard.

This synergy of all obtained knowledge is predominantly devoted to buyers in the car insurance coverage industry, who get insight into what is occurring on the highway and at the rear of the wheel. As Hari Balakrishnan, CTO and founder of CMT points out: There is a wave of impressive IoT information sources coming that will be significant to comprehending driving chance and decreasing crash fees. CMT fuses these disparate information sources to develop a unified perspective of driving.

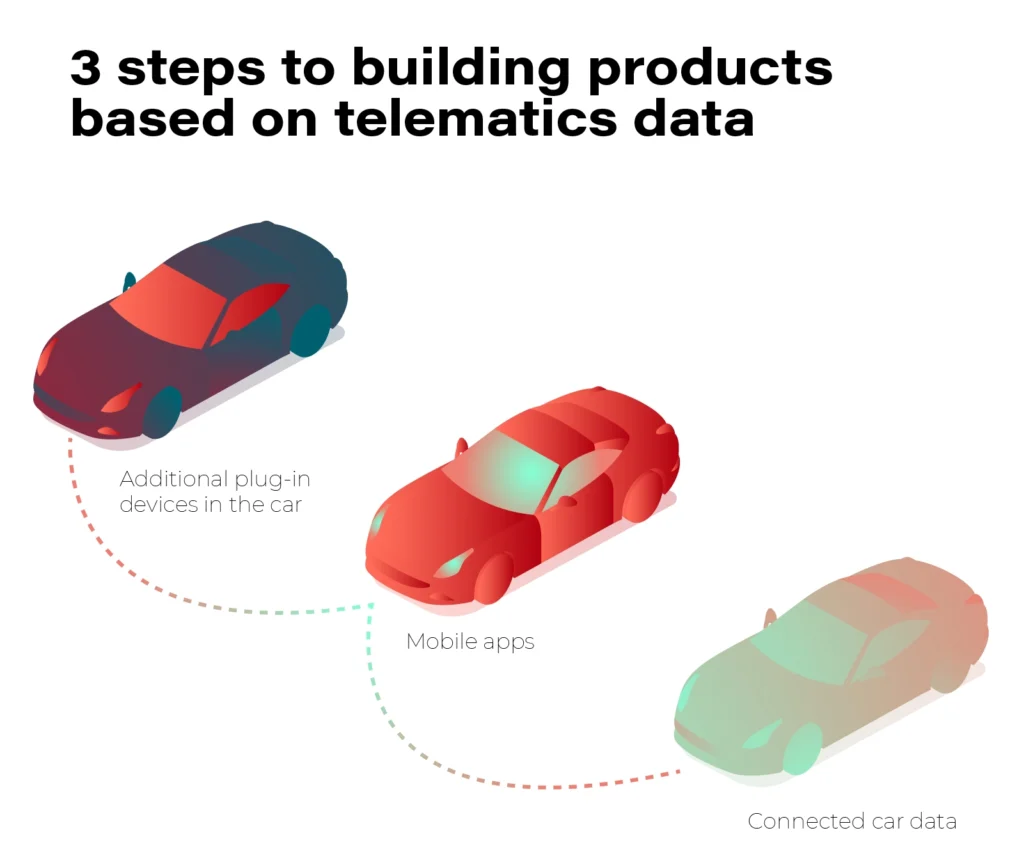

Current UBI methods can be flawed

Existing solutions of info assortment for insurers also count on modern-day technologies, but these can be unreliable. All three techniques have their drawbacks: products plugged into the On-Board Diagnostic (OBD) method, smartphone applications and tags caught to the windshield.

The to start with system presents insight into the driver’s specific behavior details, downloaded right from the engine command module (ECM). Weaknesses? The simple fact that OBD-II equipment are constrained to the info located in the ECM, for instance, when individuals from other vehicle parts keep on being inaccessible.

In this regard, cellular apps are surely superior, supplying insurers with a uncomplicated way to launch their personal telematics-primarily based program. . In addition, details is gathered each time the person drives the vehicle. The disadvantage, having said that, is that the application does not connect immediately to the vehicle’s methods. Therefore, the knowledge points are subject to a margin of error, and it also happens that the computerized driving recognition fails and features in the scoring journeys as a passenger in yet another car or truck, for illustration.

Bluetooth-based tags, which is the very last alternative explained right here, are installed on the vehicle’s windshield or rear window. Like cellular applications, the tags have no direct relationship to the vehicle’s systems and are thus inclined to bugs.

The conclusions are obvious

Hence, there is a great deal to advise that if an insurance company is searching for truly trusted know-how, it need to opt to use embedded telematics, or info. This is what enables dynamic and, earlier mentioned all, unconditional details assortment to reliably evaluate the danger involved with personal consumers.

The knowledge sent by related cars and trucks is additional precise, much more in-depth, and in considerably more substantial quantities when compared to other solutions. And this allows insurance coverage corporations to greater fully grasp buyers and their actions and, dependent on this facts, provide solutions that are far better suited to their requires, as very well as far more worthwhile.

Market insiders don’t want substantially convincing about the pros of telematics and linked vehicles in excess of other driver knowledge assortment methods. Facts from autos connected to the network are instantaneously obtainable. Of system, you can enrich it and give it context by using information from smartphones, but in most instances, it is not even important. So why commit in a little something unreliable, which by definition has vulnerabilities and does not meet up with 100 % of your needs, when you can opt for a more thorough technologies that provides far more characteristics ideal from the get started.

Considerable worth of connected car or truck knowledge for the coverage industry

Related automobile info is the subsequent action in constructing the ultimate telematics-dependent items. It is acquired with no the need to put in further components. All it takes is a vehicle user’s consent to use the facts, and then the insurance plan company obtains the data directly from the OEM.

The information and facts attained from UBI autos can be utilised correctly and all stakeholders profit: insurers, as they gain a much better knowing of their prospects and can superior evaluate risk OEMs, as it allows them to monetize the data and lastly buyers, who receive a improved, additional personalised offer this way. J.D. Electric power points out that 83% of policyholders who had positive promises encounter renewed their insurance policies, when compared to only 10% who gave adverse evaluations.

In addition, these types of trusted facts serves not only to make improvements to the profitability of an insurance plan portfolio, but also to strengthen highway security. Insurers can offer you incentives that will motivate their shoppers to constantly increase their driving model and enhance their care for by themselves and other highway end users.

Even now, current market leaders who realize the worth of investing in innovation are supplying their consumers the option to share data from related cars for UBI/BBI purposes. A single instance is the State Farm® brand, which features savings centered on driving actions. The driver’s on-the-highway habits ( sharp braking or no braking, swift acceleration, swift turns) and driving mileage are quickly sent to the info supervisor following each and every vacation, so be absolutely sure to help knowledge sharing and location products and services on your saved car or truck. This information and facts is applied to update your Generate Safe & Save price reduction each individual time you renew your policy. The safer you drive, the extra you can preserve.

Furthermore, Ford Motor Organization is progressively shifting toward applying driver info in UBI plans centered on connected vehicles. To that conclude, the automotive huge has partnered with a mobility and analytics model. Their joint project is anticipated to empower motorists with much more control around how much they shell out for their car insurance policies. Drivers can voluntarily share their driving details from activated Ford autos with Arity’s centralized telematics system, and it will then be shipped by way of Arity’s API. Drivesight® to insurers. The obtained danger index can be made use of to selling price automobile insurance coverage by any taking part insurance provider.

Presently, connected autos are only a person alternative, as a lot of insurance plan companies are even now making use of, for example, cellular programs in parallel. Having said that, we can presently see that the craze of applying CC data is existing on the market place and the variety of businesses presenting these an possibility to their clients will grow. This is a thing to be reckoned with.

Substantial positive aspects

For insurers, the advantages are tangible. In accordance to Swiss Re, with 20,000 claims managed for each yr, the average discounts soon after implementing the higher than technologies amounted to 10-30 USD for each claim.

Telematics also helps to control so-identified as claims inflation. Increasingly state-of-the-art autos are equipped with sophisticated factors, which can be high priced to exchange. Fortunately, today’s insurance company has the ability to develop its have system dependent on the switching expense of spare elements and problems history for big motor vehicle products. This permits them to produce new pricing that includes inflated payment fees.

The quicker, the better

Leveraging facts and analytics primarily based on synthetic intelligence is guaranteed to travel progress. Expanded resources of information improve the purchaser encounter and assist streamline operational processes. The positive aspects are thus apparent across the whole benefit chain. We can confidently say that never just before in history has technologies been so intertwined with the insurance coverage industry.

That’s why all insurance policy providers should start operating on incorporating related vehicle data into their programs now. The faster they do, the greater positioned they will be when this sort of automobiles come to be mainstream on the street. Right after all, the share of new motor vehicles with built-in connectivity will attain 96% in 2030.

That is what Evangelos Avramakis, Head Digital Ecosystems R&D, Swiss Re Institute Exploration & Engagement advises insurance businesses to do: Setting up tiny then scaling speedy may well be a good tactic (…) There is so a great deal you can do with details. But you need to have to take a various solution, depending on no matter whether you want to improve claims processing or generate new products. Conversely, this is what Nelson Tham, eAdmin Expert Asia, P&C Business Administration, thinks about implementations: Anytime an SME thinks about digitalization, it intimidates them. But it will need not be the scenario if we get started little. They can start by examining their inner procedures, see how facts flows, transform that into structured facts, then review this information for additional significant insights.

How the insurance policies field must method the matter?

Insurers really should get started by answering crucial questions like: exactly where linked vehicle information will provide the most price for my business? What interior capabilities do we have and need? Do we have the essential infrastructure, course of action and competencies to leverage connected motor vehicle info? What investments in technological innovation are necessary to produce on our objectives?

And lastly, they have to have to contemplate irrespective of whether they can much better and a lot quicker accomplish those people goals by constructing essential abilities in-home or doing work with associates.

A great business and technological know-how partner for the coverage field is fundamental

Working with connected auto information is not that uncomplicated. It calls for know-how and the right technological know-how qualifications, as nicely as locating the right spouse to collaborate with.

A properly-matched companion will aid transform the present-day running design, by combining automotive and know-how competencies and at the identical time comprehension the specifics of the insurance coverage market. Some procedures simply just have to be carried out in a thorough and holistic way.

At GrapeUp, we assist apply new techniques to an current strategy. Operating at the intersection of automotive and coverage, we focus in the systems of tomorrow. Call us if you want to boost your business efficiency.

[ad_2]

Resource url